What is a Credit Score?

When it comes to managing your finances, one number can have a huge impact on your future: your credit score. But what exactly is a credit score, how is it calculated, and why does it matter so much? If you’re new to credit or just want to understand how it works, this guide breaks it down in simple, actionable terms.

For more tips on building your credit from scratch, check out our comprehensive guide here.

Understanding Your Credit Score

A credit score is a three-digit number that represents your creditworthiness. Lenders, landlords, and even some employers use it to evaluate how responsible you are with money. Simply put, your credit score is a snapshot of your financial behavior and reliability when borrowing money.

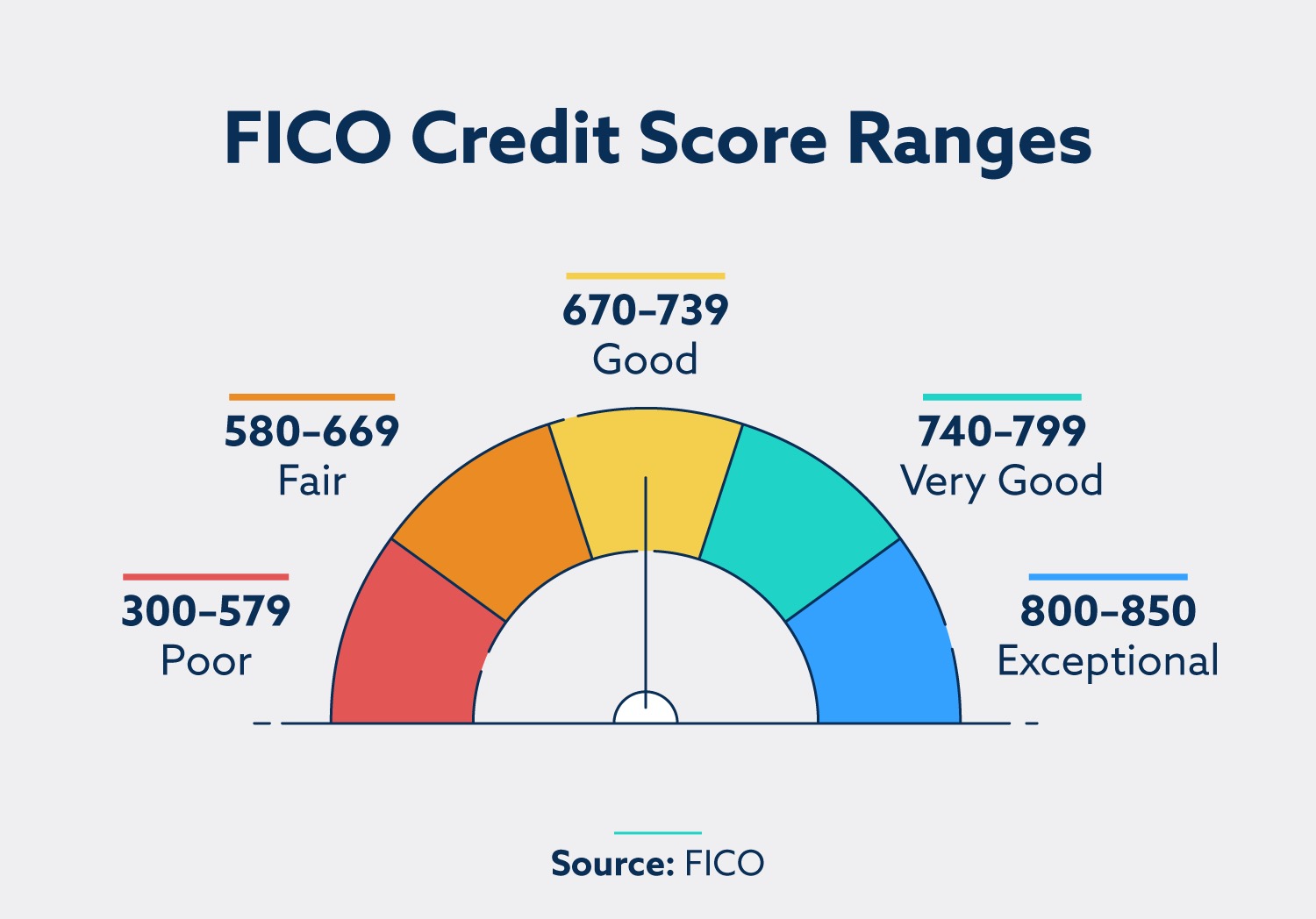

Credit scores generally range from 300 to 850:

- Poor: 300–579

- Fair: 580–669

- Good: 670–739

- Very Good: 740–799

- Excellent: 800–850

The higher your score, the more confident lenders feel that you will repay your debts responsibly.

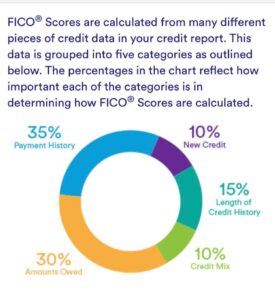

How Credit Scores Are Calculated

Your credit score isn’t random—it’s based on several factors that collectively reflect your financial habits.

Payment History (35%)

Payment history is the most significant factor affecting your score. It shows whether you’ve paid bills and loans on time. Late payments, collections, and bankruptcies can negatively impact this portion of your score. Consistently paying bills on time is the most effective way to build a positive credit history over time.

Amounts Owed / Credit Utilization (30%)

This factor measures how much of your available credit you’re using. For example, if your credit card limit is $2,000 and your balance is $500, your credit utilization is 25%. Experts recommend keeping utilization below 30% of your total credit limits, ideally even lower, without letting it drop to 0%, which can limit scoring potential.

Length of Credit History (15%)

The age of your credit accounts contributes to your score. Older accounts demonstrate financial experience and responsibility. This includes the age of your oldest and newest accounts, and the average age of all accounts. Simply keeping accounts open and in good standing over time can steadily improve this factor.

New Credit (10%)

Every time you apply for new credit, it triggers a hard inquiry, which can temporarily lower your score. Multiple applications in a short period can compound the effect. To minimize impact, rate shop loans, like mortgages or auto loans, within a short window (usually 14–45 days) so inquiries are consolidated.

Credit Mix (10%)

Credit mix refers to the variety of credit accounts you have, such as credit cards, auto loans, student loans, and mortgages. A diverse mix demonstrates your ability to manage different types of credit responsibly. However, don’t open unnecessary accounts just to diversify—responsible management matters more than variety.

Why Your Credit Score Matters

Your credit score affects more than just loan approvals. It influences many areas of your financial life:

- Loan approvals and interest rates: Higher scores usually mean better rates and more loan options.

- Renting an apartment: Landlords may check your score to ensure you’re a reliable tenant.

- Insurance premiums: Some insurers use credit scores to calculate rates.

- Employment background: Certain employers review credit history for financial responsibility roles.

How to Check Your Credit Score Safely

Knowing your credit score is the first step toward understanding your financial health. Checking your score yourself is a soft inquiry and does not hurt your credit.

- Access free reports from the major bureaus: Experian, Equifax, and TransUnion.

- Use MyFICO for an official FICO score.

- Monitor your score regularly to catch errors and track improvements.

Common Misconceptions About Credit Scores

Credit scores can be confusing, and myths abound. Here are a few common misconceptions:

- Closing accounts always improves your score: Not necessarily—closing old accounts can shorten your credit history.

- Checking your own score lowers your score: False, only hard inquiries from lenders affect your score.

- Paying off a debt immediately erases all history: The positive payment history still benefits your score.

Using Your Credit Score to Make Better Financial Decisions

Understanding your credit score empowers you to make smarter financial choices. Here are practical ways to leverage this knowledge:

- Plan for loans or mortgages and avoid unnecessary applications.

- Focus on consistent on-time payments and keeping balances low.

- Budget responsibly and prioritize paying high-interest debts first.

FAQs About Credit Scores

What is considered a good credit score?

Generally, a score above 670 is considered good, while 740+ is very good or excellent. Scores below 580 are poor and may limit borrowing options.

How often can I check my credit score for free?

You can check your credit report for free weekly from AnnualCreditReport.com. Some services like Experian and Credit Karma also provide ongoing free access.

Can my credit score go up quickly?

Significant improvements usually take several months of consistent responsible behavior. Paying down balances and making on-time payments are the fastest ways to see positive changes.

Do all lenders use the same credit score model?

No, different lenders may use FICO, VantageScore, or proprietary models. Scores can vary slightly depending on the source.

How long does negative information stay on my credit report?

Most negative items, like late payments, stay for 7 years, while bankruptcies can remain up to 10 years. Responsible behavior can help offset these impacts over time.

Conclusion

Your credit score is more than just a number—it’s a reflection of your financial habits and a key factor in many aspects of your life. Understanding how it works allows you to make informed decisions, monitor your progress, and plan for your financial future. Whether you’re just starting or looking to improve, knowledge is the first step toward financial empowerment.

For actionable steps on how to build credit from scratch, be sure to check out our detailed guide here.