Monitoring your personal credit is an essential part of managing your financial health, but many people are unsure where to start. You might wonder, “How can I check my credit without paying a fortune for it?” The good news is that there are several ways to monitor your personal credit for free. Whether you’re aiming to improve your credit score, planning to apply for a loan, or simply want to safeguard against identity theft, keeping an eye on your credit is a smart move.

In this beginner-friendly guide, we’ll explore everything you need to know about monitoring your personal credit for free. Let’s get started!

What Is a Credit Report and Why Does It Matter?

Before diving into how to monitor your credit, it’s important to understand what a credit report is and why it plays such a vital role in your financial life.

Credit Report Basics

Your credit report is essentially a summary of your financial history. It includes detailed information about your credit accounts, payment history, the amount of debt you owe, and any public records, such as bankruptcies. This report is created by three major credit bureaus: Equifax, Experian, and TransUnion. These agencies collect and update your credit information regularly.

Credit Score Overview

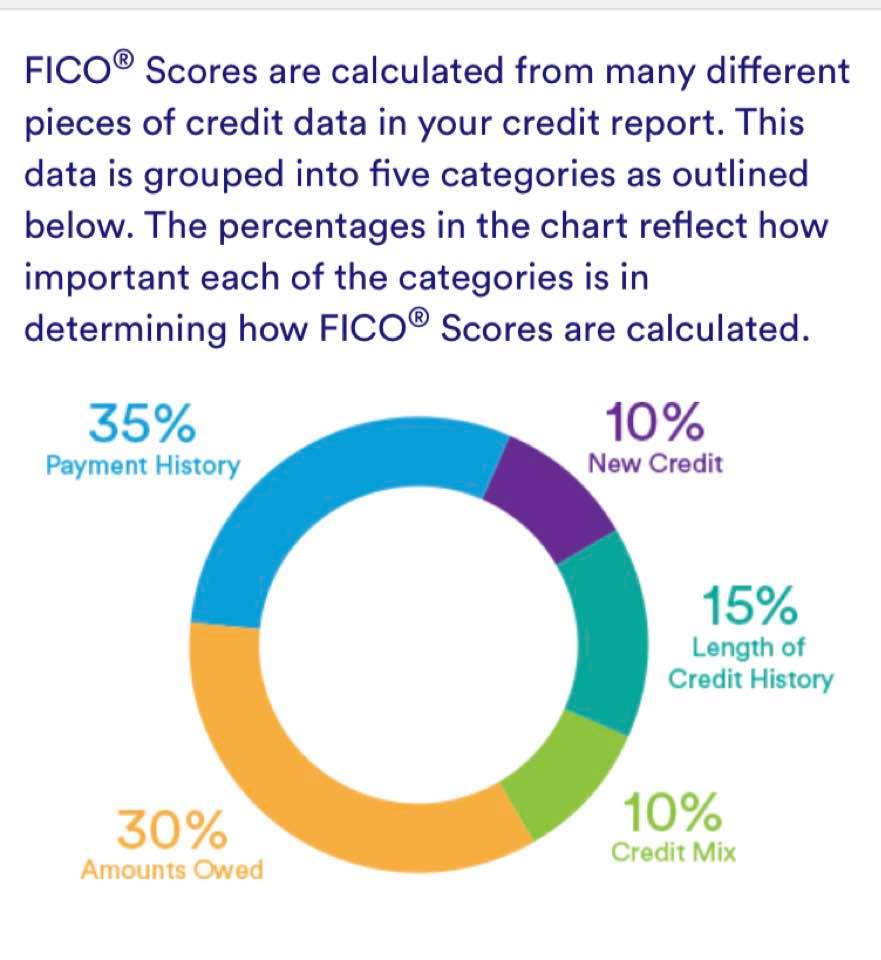

In addition to your credit report, you have a credit score. This three-digit number reflects your creditworthiness. Scores typically range between 300 and 850, with higher scores indicating better credit health. Your score is calculated based on several factors, including your payment history, amounts owed, length of credit history, types of credit used, and new credit inquiries.

It’s worth noting that each of the three credit bureaus calculates your score slightly differently, so you may see variations in your score depending on where you check it.

Why Monitoring Your Credit is Essential

Monitoring your credit regularly helps you stay on top of your financial situation. Here are some key reasons why it’s important:

- Early Detection of Fraud: If someone tries to steal your identity or open fraudulent accounts in your name, credit monitoring can alert you early so you can take action.

- Applying for Loans: Whether you’re buying a house, financing a car, or applying for a credit card, lenders use your credit score to determine your creditworthiness.

- Improving Financial Health: Monitoring your credit helps you spot areas where you can improve, such as paying down debt or making payments on time, which can positively affect your score over time.

How to Get Your Credit Report for Free

Now that you understand why monitoring your credit is important, let’s look at how to obtain your credit report without paying a dime.

AnnualCreditReport.com: The Government-Authorized Source

By law, you’re entitled to a free credit report from each of the three major credit bureaus every 12 months. The best place to obtain these reports is through AnnualCreditReport.com, which is the only official, government-authorized website for free credit reports.

How to Access Your Free Credit Report

- Visit the website: Go to AnnualCreditReport.com.

- Provide your details: You’ll need to enter some personal information, such as your Social Security number and date of birth.

- Select your reports: You can choose to get a report from Equifax, Experian, and TransUnion, or just one. It’s often a good idea to spread them out over the year so you can monitor your credit consistently.

- Review your report: Once you have your report, go through it carefully.

What to Look for in Your Credit Report

When reviewing your credit report, pay attention to the following:

- Errors: Check for any inaccuracies in your personal information (such as wrong addresses) or accounts you don’t recognize.

- Closed Accounts: Make sure any accounts you’ve closed are listed correctly.

- Inquiries: Look at the section detailing who has checked your credit. If you spot an inquiry you don’t recognize, it could be a sign of fraud.

Free Credit Monitoring Tools and Services

While you can get your credit report for free once a year, staying informed in real-time requires a bit more help. Luckily, several free credit monitoring tools make this easy.

Free Credit Score vs. Full Credit Report

It’s important to know the difference between checking your credit score and accessing a full credit report. Free credit monitoring tools often provide access to your credit score but may not include your full report unless you pay for premium services. However, tracking your score can give you a good idea of your overall financial health.

Top Free Credit Monitoring Tools

Here are some of the most popular free tools for monitoring your credit:

- Credit Karma: Offers free credit scores from two major credit bureaus (Equifax and TransUnion) and real-time credit monitoring. Credit Karma also provides tips on how to improve your score.

- Credit Sesame: This tool provides free access to your credit score and offers recommendations on how to improve your credit. Credit Sesame also offers identity theft protection and monitoring services.

- Experian Free Credit Monitoring: With Experian’s free monitoring service, you can get access to your Experian credit score, as well as alerts whenever there are major changes to your report.

- Mint: A personal finance app that tracks your credit score for free and helps you manage your finances by tracking spending, creating budgets, and monitoring bills.

How These Tools Work

After signing up, these tools continuously monitor your credit and send you real-time alerts for any major changes, such as new accounts being opened or credit inquiries made in your name. This helps you stay informed and take quick action if anything looks suspicious.

Tips for Maintaining a Healthy Credit Score

Monitoring your credit is just one part of the equation. To keep your credit in good standing, you also need to practice good credit habits.

Understanding What Affects Your Credit Score

Here are the key factors that impact your credit score:

- Payment History: Making payments on time is the most critical factor. Late or missed payments can significantly hurt your score.

- Amounts Owed: High balances on credit cards or loans relative to your credit limit can lower your score.

- Length of Credit History: A longer credit history tends to improve your score.

- Types of Credit: Having a mix of credit types, such as credit cards, mortgages, and installment loans, can positively affect your score.

- New Credit: Frequently applying for new credit can hurt your score, especially if there are many hard inquiries in a short period.

Best Practices for Maintaining Good Credit

- Pay Bills on Time: Always make at least the minimum payment by the due date.

- Keep Credit Utilization Low: Try to use less than 30% of your available credit. If possible, keep your balance under 10%.

- Limit Hard Inquiries: Only apply for new credit when you really need it.

- Regularly Review Your Credit Report: Even if everything looks fine today, check your report at least once a year to catch any errors or signs of identity theft.

Dealing with Errors on Your Credit Report

If you spot an error, don’t panic. You can file a dispute with the credit bureau that provided the report. Most bureaus allow you to submit disputes online, and they are required by law to investigate and correct any inaccuracies.

Avoiding Scams and Paid Credit Monitoring

With so many free resources available, it’s important to avoid falling for scams or paying for services that you don’t need.

Warning Signs of Credit Monitoring Scams

Be cautious of companies that:

- Make big promises: If a service claims to improve your credit score overnight or remove negative information from your report, be wary.

- Require upfront payments: Legitimate services won’t ask for fees just to monitor your credit.

How to Avoid Being Scammed

Stick to reputable, well-known companies like Credit Karma, Credit Sesame, and AnnualCreditReport.com. These services are free and don’t require sensitive information beyond what is necessary to verify your identity.

Conclusion

Monitoring your personal credit is an important step toward achieving financial stability. It doesn’t have to be complicated or costly. By regularly checking your credit report and using free credit monitoring tools, you can stay informed, spot potential issues early, and take control of your financial future. Start today by visiting AnnualCreditReport.com or signing up for one of the free tools we’ve mentioned.

FAQ

1. How often should I check my credit report?

You’re entitled to a free credit report from each of the three major bureaus every 12 months. To monitor your credit consistently, consider checking one bureau’s report every four months.

2. Will checking my credit hurt my score?

No, checking your own credit report or score is considered a “soft inquiry” and does not affect your credit score.

3. What is the difference between a credit score and a credit report?

A credit report provides detailed information about your credit history, while a credit score is a numerical representation of your creditworthiness.

4. What should I do if I find an error on my credit report?

If you find an error, you should file a dispute with the credit bureau that issued the report. They are required by law to investigate and correct any inaccuracies.

5. Are free credit monitoring services safe?

Yes, reputable services like Credit Karma, Credit Sesame, and AnnualCreditReport.com are safe to use and offer real-time alerts to help you monitor your credit.