Understanding your credit score can feel like navigating a labyrinth. With so many factors influencing your score, it’s easy to get overwhelmed. However, grasping what impacts your credit score is crucial for anyone looking to achieve financial stability, secure loans, or simply improve their overall financial health. In this blog post, we’ll break down the key components that affect your credit score, offering practical advice and insights to help you manage and improve your score effectively.

WHAT IS A CREDIT SCORE?

A credit score is a three-digit number that lenders use to assess your creditworthiness. Ranging from 300 to 850, your score summarizes your credit history, payment behavior, and overall financial reliability. The higher your score, the more trustworthy you appear to lenders, which can lead to better loan terms, lower interest rates, and higher credit limits.

WHY DOES YOUR CREDIT SCORE MATTER?

Your credit score plays a significant role in various financial aspects of your life. It can affect your ability to:

– Qualify for loans or credit cards

– Secure favorable interest rates

– Rent an apartment

– Get insurance at a lower rate

– Even land a job in some cases

Understanding what impacts your credit score can empower you to make informed financial decisions.

KEY FACTORS THAT IMPACT YOUR CREDIT SCORE

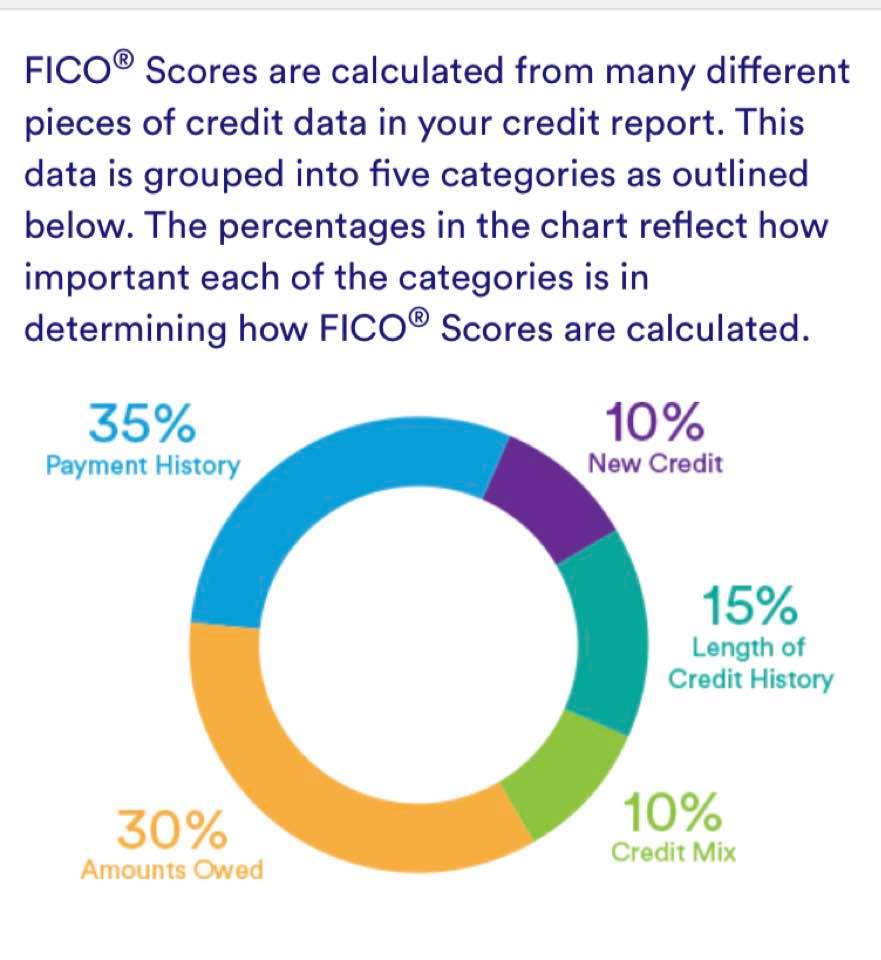

1. PAYMENT HISTORY

Your payment history is one of the most significant factors affecting your credit score, making up about 35% of the total score. This section reflects whether you’ve paid your bills on time, including credit cards, mortgages, and other loans. A consistent record of timely payments can boost your score, while missed or late payments can severely damage it.

To maintain a good payment history, consider setting up automatic payments or reminders. This strategy can help you avoid late payments and keep your score healthy.

2. CREDIT UTILIZATION

Credit utilization accounts for around 30% of your credit score. This metric measures how much of your available credit you are using. Ideally, you should aim to keep your credit utilization ratio below 30%. For example, if you have a total credit limit of $10,000, try to keep your outstanding balance under $3,000.

To improve your credit utilization, you can pay down existing debt or request a credit limit increase. Just be cautious with the latter; increased limits can be beneficial, but it’s essential not to increase your spending habits.

3. LENGTH OF CREDIT HISTORY

The length of your credit history makes up about 15% of your credit score. This factor considers how long your credit accounts have been active. A longer credit history can portray you as a more reliable borrower. If you have older accounts, keeping them open (even if you don’t use them) can positively impact this aspect of your score.

If you’re new to credit, consider becoming an authorized user on a family member’s or friend’s account. This strategy can help you establish a credit history without taking on significant debt.

4. TYPES OF CREDIT IN USE

The types of credit you have also contribute to your score, accounting for about 10% of the total. A healthy mix of credit accounts—such as credit cards, mortgages, and installment loans—can enhance your credit profile. Lenders want to see that you can manage various types of credit responsibly.

To diversify your credit, consider applying for different types of accounts. However, be cautious not to apply for too much credit at once, as doing so can negatively impact your score.

5. NEW CREDIT INQUIRIES

New credit inquiries, which make up about 10% of your score, occur when you apply for new credit. Each application results in a hard inquiry on your credit report, which can temporarily lower your score. While it’s essential to be proactive in seeking credit, try to limit applications to avoid multiple inquiries in a short period.

If you’re shopping for a loan, such as a mortgage or auto loan, try to do so within a short timeframe. Many scoring models treat multiple inquiries in a short span as one inquiry, reducing the potential negative impact on your score.

CONCLUSION

Understanding what impacts your credit score is vital for managing your financial health. By focusing on key areas like payment history, credit utilization, and the length of your credit history, you can take actionable steps to improve your score. Remember, building a good credit score takes time and consistency, but the benefits are well worth the effort.

Regularly check your credit report and score to track your progress and make adjustments as needed. With a solid grasp of your credit score’s components, you can make informed financial choices that lead to a brighter financial future.

FREQUENTLY ASKED QUESTIONS

What is considered a good credit score?

A good credit score typically ranges from 700 to 749. Scores above 750 are considered excellent, while scores below 600 are generally viewed as poor. However, different lenders may have varying thresholds for what they consider acceptable.

How often should I check my credit score?

You should check your credit score at least once a year to stay informed about your financial health. Some services allow you to check your score monthly for free, which can help you track changes over time.

Can I improve my credit score quickly?

While significant improvements take time, you can see small changes in your score relatively quickly by paying down debt, making on-time payments, and reducing your credit utilization.

Does closing a credit card hurt my score?

Yes, closing a credit card can hurt your score by reducing your available credit and affecting your credit utilization ratio. If the card has a long credit history, it may also shorten your overall credit age.

How long does negative information stay on my credit report?

Most negative information, such as late payments or collections, can stay on your credit report for up to seven years. However, bankruptcies can remain for up to ten years. It’s essential to maintain positive habits to offset any negative marks.

By understanding and managing these factors, you can improve your credit score and secure a more favorable financial future.